CGT Other Disposals

This guide explains how to use the My Tax Digital interface to record Capital Gains Tax (CGT) on the disposal of assets other than UK residential property — including cryptoassets, listed and unlisted shares, and other chargeable assets.

These disposals are reported on SA108 (Capital Gains Summary).

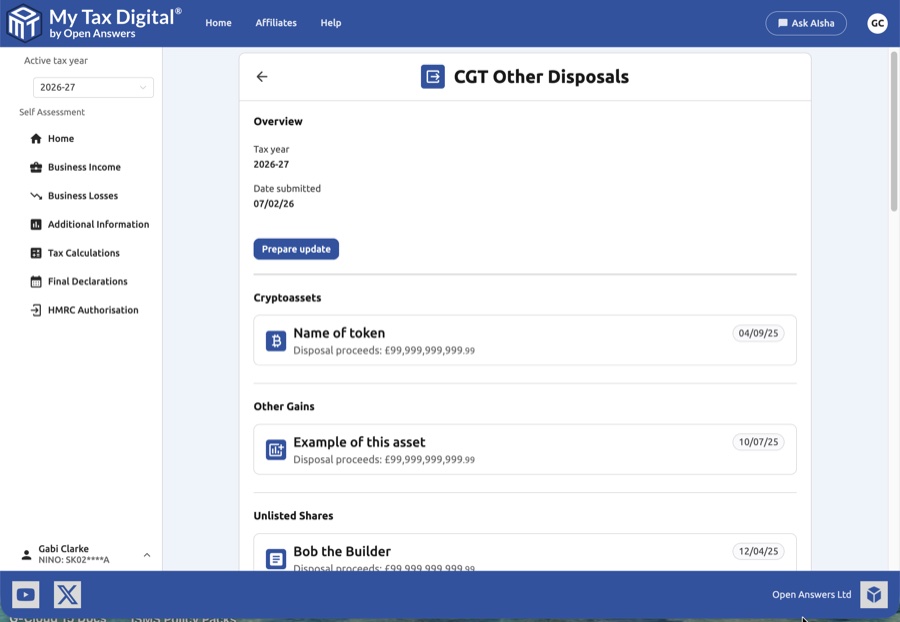

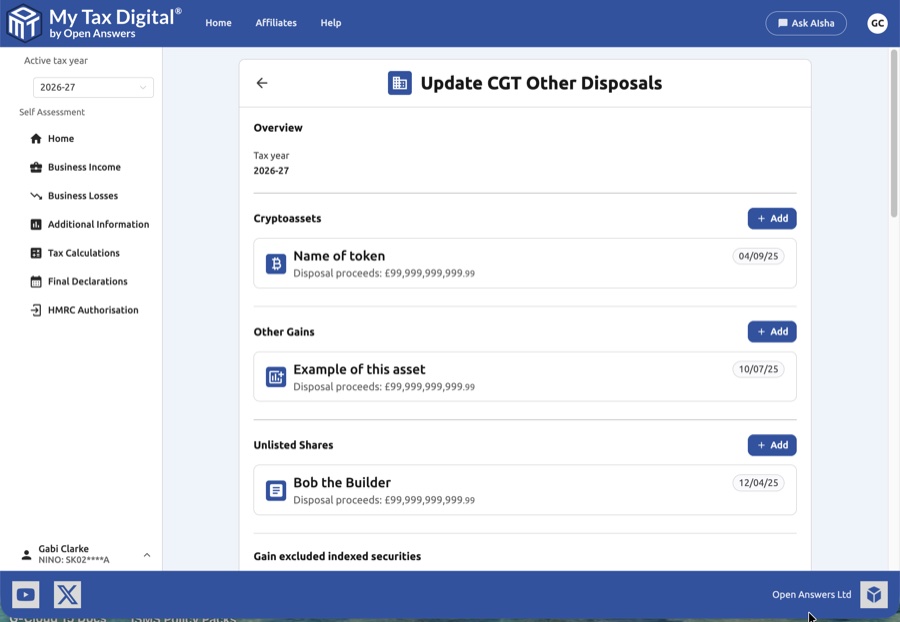

1. The CGT Other Disposals Overview

The CGT Other Disposals screen categorises your disposals by asset type.

- Asset Categories: The screen is divided into sections for different asset types:

- Cryptoassets: Disposals of cryptocurrency and other digital assets.

- Other Gains: Disposals of other chargeable assets (e.g., personal possessions above the threshold, commercial property, or other investments).

- Unlisted Shares: Disposals of shares in companies not listed on a recognised stock exchange.

- Existing Entries: Each entry shows the asset name, disposal proceeds, and disposal date.

- Gain Excluded Indexed Securities: A section at the bottom for gains on indexed securities that are excluded from CGT calculations.

- Prepare Update: Click the Prepare update button to enable editing and add new disposal entries.

2. Adding a Disposal

Click the + Add button next to the relevant asset category to open the disposal entry modal.

| Field | Description | SA108 |

|---|---|---|

| Asset name / description | The name or description of the asset disposed of. | — |

| Company name | Optional. The name of the company whose shares/asset was disposed of. | — |

| Company registration number | Optional. Only accepts a UK Companies House format (8 digits, or 2 letters followed by 6 digits) — this is an HMRC requirement, not a My Tax Digital restriction. For a non-UK company, leave this field blank; it is not required to save or submit the entry. | — |

| Disposal date | The date of the disposal. | — |

| Disposal proceeds | The total amount received (or market value if gifted). | Box 6 |

| Acquisition date | The date the asset was originally acquired. | — |

| Acquisition amount | The original cost of the asset. | Box 7 |

| Improvement costs | Any capital improvements made to the asset. | Box 7 |

| Additional costs | Other allowable costs (e.g., professional fees, transaction costs). | Box 7 |

| Losses from this year | Current year losses being offset against this gain. | — |

| Losses from previous year | Losses brought forward from earlier years. | — |

| Amount of net gain | The final net gain after costs and losses. | Box 6 |

| Gains with BADR | The portion qualifying for Business Asset Disposal Relief. | — |

| Gains with INV | The portion qualifying for Investors' Relief. | — |

3. Asset-Specific Guidance

Cryptoassets

Each disposal of cryptocurrency (e.g., Bitcoin, Ethereum, NFTs) is a separate CGT event. Use the pooling rules for fungible tokens — your cost basis is typically calculated using HMRC's Section 104 pool method. Record each disposal separately.

Unlisted Shares

Shares in private (unlisted) companies are valued at market value on acquisition and disposal. You may need a professional valuation if no arm's length transaction occurred.

Other Gains

Use this category for any other chargeable asset not covered above, such as:

- Commercial property

- Personal possessions worth more than £6,000 (the chattel exemption)

- Antiques, artwork, or collectibles

- Business goodwill

4. Finalising Your Submission

After entering all disposals:

- Submit / Update: Save your entries to include them in your SA108 return.

- Delete Entry: Use the red Delete link inside a modal to remove a specific record.

- Cancel: Discard changes and return to the overview.